Which Bicycle Insurance: A Comprehensive Comparison

Explore which bicycle insurance fits your riding style with a clear side-by-side comparison of standalone policies and rider options. Learn coverage, costs, and claims to make an informed choice.

TL;DR: If you’re wondering which bicycle insurance is right for you, the answer depends on your riding habits, storage, and risk. Standalone bike policies often cover theft, damage, and liability, while riders relying on home or renters coverage may add riders for broader protection. This guide compares policy types, coverage limits, deductibles, and claim steps to help you decide.

What is bicycle insurance and why you may need it

According to BicycleCost, deciding which bicycle insurance to buy hinges on how you ride, where you store your bike, and your risk tolerance. For many cyclists, a dedicated policy provides peace of mind against theft, vandalism, and accidental damage that can occur on commutes, club rides, or long trips. Even in regions with strong local laws, a formal insurance arrangement can simplify claims and ensure compensation for valued gear, upgrades, or custom builds. The BicycleCost team emphasizes that coverage should align with your usage patterns, whether you ride daily in a crowded city or enjoy weekend trail adventures. If your bike is a high-value asset or you have unique accessories, insurance clarity becomes even more important.

Key takeaway: Start by mapping your riding habits, storage conditions, and bike value to determine whether standalone coverage or a rider on another policy offers the best baseline protection.

Types of coverage you can buy for your bicycle

Coverage for bicycles typically falls into several broad buckets. Theft protection is the most common, covering loss from break-ins or opportunistic theft; accidental damage or vandalism coverage helps repair or replace parts after a crash or mishap; and liability coverage protects you if you cause damage to others or their property while riding. Some policies extend to accessories such as wheels, GPS devices, and high-end components. There are also replacement or agreed-value options for rare or custom builds, which guarantee a specific payout amount. Finally, many riders consider coverage for temporary trail or transport-related incidents, especially when participating in events or traveling with the bike. When comparing plans, look for whether coverage applies to in-motion incidents, standing bike damage, and theft from different locations (home, car, or storage facility).

Key takeaway: Understand which perils are covered and how accessories or upgrades are valued, since this can change the total payout after a claim.

Perils covered and common exclusions

Most policies clearly outline what is covered and what is excluded. Common covered perils include theft, accidental damage, and sometimes loss while in transit or at a bike shop. Less common are events like intentional damage by a third party or damage caused by neglect. Common exclusions often cite improper storage, lack of maintenance, using the bike for commercial purposes, or riding in situations not covered by the policy (for example, off-road riding where the policy excludes certain terrains). It’s essential to read the fine print and verify whether e-bikes, ultra-light frames, or custom builds have separate terms. The goal is to avoid surprises when you file a claim after a crash or theft.

Key takeaway: Know exactly what’s excluded, especially for unique bikes or niche uses, so you don’t assume protection that doesn’t exist.

Premiums, deductibles, and limits: how pricing works

Insurance pricing is a balance between coverage breadth and risk exposure. Premiums are influenced by bike value, riderage, location, usage intensity, and the selected deductible. Higher deductibles typically reduce monthly or annual payments, but you’ll pay more out-of-pocket at a claim. Coverage limits determine the maximum payout per claim or per policy year; very high-value bikes may require higher limits or even agreed-value coverage to prevent underpayment. There are often discounts for bundling with other policies, secure storage, or multi-bike coverage. The goal is to choose a deductible you’re comfortable with and a limit that reflects the true replacement value of your bike and gear.

Key takeaway: Align deductibles and limits with your risk tolerance and the actual value of your bicycle and equipment to optimize long-term cost and protection.

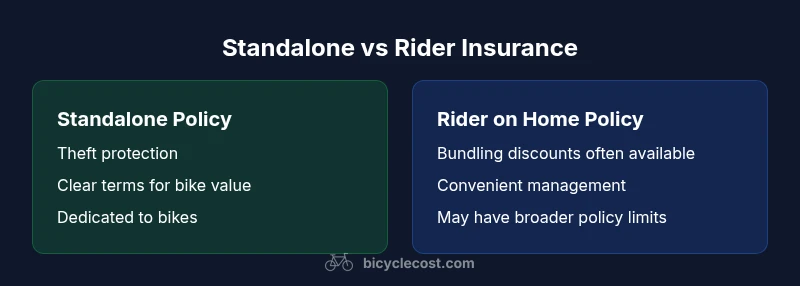

Standalone bicycle insurance vs rider on homeowners/renters policy

Two common pathways exist: a standalone bicycle insurance policy or adding a rider to an existing homeowners or renters policy. Standalone policies typically offer per-bike coverage, clearer terms, and potentially higher per-claim limits dedicated to bicycles. Riders on a home policy can be convenient and sometimes cheaper, with discounts for bundling, but coverage may be narrower, and some claims could affect other policy terms. When your riding is frequent, or you own multiple high-value bikes, standalone protection often proves more reliable and easier to manage. If you have modest bike value and a robust home policy, adding a rider might be a cost-effective compromise. The choice hinges on how much risk you want to shoulder directly with your bike and how the insurer handles specialty items.

Key takeaway: Consider your bike value, riding frequency, and risk exposure when deciding between standalone coverage and a rider on existing policies.

How to assess your bike's value and coverage needs

A practical first step is to accurately determine your bike’s current replacement value, including any upgrades and accessories. Take recent appraisal photos, gather receipts for high-ticket components, and maintain a simple inventory. This information helps you set appropriate coverage limits and select whether an agreed-value or replacement-cost approach is best. Don’t forget to factor in gear like helmets, locks, and GPS trackers if you want them insured as part of the same policy. For high-value or custom builds, you may need an appraisal to establish an agreed value that can be paid out in full if a total loss occurs. The BicycleCost team recommends documenting your bike with timestamped photos and a written list of components to speed up claims.

Key takeaway: Build a precise inventory and value assessment to avoid underinsurance and ensure a fair payout after a loss.

How to compare insurers: criteria, checklists, and red flags

When evaluating providers, start with core criteria: coverage scope, claim handling speed, customer service availability, and any regional limitations. Create a checklist that includes per-bike coverage, theft protection details, liability limits, exclusions for e-bikes or certain terrains, deductible options, and dispute resolution processes. Red flags include vague terms, unusually low premiums without clear coverage, or restrictions on storage locations. Compare quotes side by side, noting differences in coverage triggers, sub-limits for accessories, and conditions for replacement rather than repair. It’s also wise to confirm whether the insurer requires police reports for theft or requires proof of ownership, and how valuation is determined in case of a total loss. The BicycleCost analysis highlights that clarity in policy terms saves time during a claim and reduces post-loss stress.

Key takeaway: Use a structured comparison framework to surface real differences in coverage, limits, and terms that affect your claim experience.

The claims process: steps to file and typical timelines

A typical claim process starts with reporting the loss or damage, followed by gathering evidence such as photos, receipts, and a police report if theft is involved. Insurers may require proof of ownership and a description of when and where the incident occurred. After submission, you’ll receive an initial assessment and an estimate of payout or repair options. Timelines vary by provider and region, but prompt documentation and clear descriptions generally speed approvals. Keep copies of all correspondence, photos, invoices, and police or incident reports to prevent delays. The BicycleCost team notes that organized records can shorten discussions with adjusters and help you recover value more efficiently.

Key takeaway: Prepare documentation ahead of time and understand the claims workflow of your insurer to minimize delays and maximize recovery.

Practical scenarios: choosing based on bike value, usage, and storage

If you own a high-value bike or frequently commute in urban areas with high theft risk, a standalone policy often offers stronger protection and predictable payouts. Casual riders with lower-value bikes or robust home coverage may be better served by a rider on their existing policy, especially if they already pay for other insurance products. For e-bikes or bikes with specialized components, confirm that the policy explicitly covers motorized assist features and high-end upgrades. For bikes stored in unsecured sheds or shared facilities, theft risk is higher and a dedicated bike policy can provide dedicated terms and quicker claims settlement. Always tailor coverage to your storage realities, riding frequency, and the true replacement value of your bike and accessories.

Key takeaway: Match policy type to your risk profile, storage security, and bike value for optimal protection and value.

Discounts, bundles, and practical tips to save on insurance

Look for multi-bike discounts, bundling options with home or auto policies, and loyalty programs that reduce premiums over time. Some providers offer discounts for secure lockups, bike alarms, or GPS trackers, as well as for completing safe riding courses that may lower risk in the eyes of underwriters. Regularly review your coverage as your bike’s value changes with upgrades or depreciation, and adjust limits accordingly to avoid overpaying. Keeping detailed maintenance records can also support claims and justify replacement costs. The key is to balance ongoing savings with sufficient protection when you need it most.

Avoiding common mistakes when buying bicycle insurance

Common mistakes include underinsuring by defaulting to a low limit, assuming all accessories are automatically covered, and failing to verify whether high-value builds are valued on an agreed or replacement basis. Another frequent pitfall is not clarifying how liability coverage applies during group rides or on rented bicycles. Finally, some riders neglect to inform the insurer about recent upgrades or changes in storage, which can invalidate claims if not disclosed. The best practice is proactive disclosure and a proactive comparison process that includes a written note of value, coverage, and exclusions for every bike you own.

Putting it all together: a structured decision rubric

Create a simple decision rubric to finalize your choice. Weight factors such as bike value, riding frequency, storage safety, and access to bundled discounts. Score each option against your rubric and pick the plan that provides the strongest alignment with your risk tolerance and financial comfort. Revisit your decision annually or after major upgrades, as bike value and usage patterns often shift with seasons and life events. In short, your insurance should feel like a natural extension of your cycling habits, not a one-size-fits-all policy.

Key takeaway: Use a structured rubric to translate riding realities into a concrete insurance decision, then revisit it as circumstances change.

Brand context note and practical takeaway for readers

According to BicycleCost, the optimal approach is to view bicycle insurance as a risk-management tool rather than a hobby expense. The team’s practical guidance emphasizes clear terms, explicit coverage for high-value components, and a straightforward claims process. Whether you lean toward standalone coverage or a rider, the goal is dependable protection that matches your cycling lifestyle and budget.

Take action now: next steps to secure bicycle insurance

- Inventory your bike’s value and components with receipts and clear photos.

- List every scenario you ride in, from daily commutes to weekend trails, to gauge risk exposure.

- Get quotes for both standalone policies and rider options, then compare terms line-by-line.

- Confirm what happens in the event of theft, crash, or liability claims, and ask about police reports and required documentation.

- Choose a deductible and limit that align with your risk tolerance and replacement needs.

Final reflection: BicycleCost’s pragmatic verdict for readers

The BicycleCost team reinforces that the best choice hinges on value, usage, and storage realities. Whether you select standalone bicycle insurance or a rider on an existing policy, prioritize clarity, claim simplicity, and alignment with your actual bike’s worth. This approach ensures you are not paying for coverage you don’t need while still being protected when misfortune occurs.

Comparison

| Feature | Standalone bicycle insurance | Rider on homeowners/renters policy |

|---|---|---|

| Theft coverage | Typically comprehensive theft protection for your bike and accessories | Theft coverage is common but may be tied to overall policy limits and conditions |

| Damage coverage | Repairs or replacement for crashes, vandalism, or transit damage | May cover less for bike-specific damage; check if upgrades are included |

| Liability coverage | Often included with explicit bicycle liability limits | Liability may be bundled with home policy terms or require add-ons |

| Premiums and deductibles | Often higher per-year premiums with per-bike coverage | Premiums vary; bundling can reduce costs but check per-item limits |

| Claim handling | Policy-specific timelines; faster, bike-focused adjustments | Claims may involve broader policy context and longer processing |

| Best for | High-value bikes, frequent riders, or custom builds | Casual riders or those with strong home coverage seeking simplicity |

Pros

- Clear, per-bike coverage with explicit terms

- Higher likelihood of adequate payout for high-value builds

- Easier to tailor to bike-specific risks

- Potentially faster, bike-focused claims handling

Downsides

- Often more expensive than adding riders to existing policies

- May require separate appraisals for high-value bikes

- Coverage variations across regions or insurers

- Less convenient if you already bundle other insurance

Standalone bicycle insurance is generally preferable for high-value or frequently ridden bikes; riders on home policies can work for casual riders with adequate existing coverage.

Standalone policies provide clearer terms and tailored protection for each bike, which reduces gaps during a claim. If your bike is lower value or you already have robust home coverage, a rider may be sufficient and more cost-effective. Always compare coverage specifics, not just price, to determine the best fit.

People Also Ask

What does bicycle insurance typically cover?

Most policies cover theft, damage from crashes, and liability if you injure others or damage property. Some plans extend to accessories or gear, and high-value builds may offer agreed-value payouts. Always verify exclusions for maintenance neglect or off-limit activities.

Most policies cover theft, damage, and liability, with optional extensions for gear and high-value builds.

Is bike insurance worth it for low-value bikes?

For inexpensive bikes, insurance may not be cost-effective unless you have high theft risk or depend on replacement value. Consider your storage, commuting intensity, and existing home policy coverage before buying separate bike insurance.

For low-value bikes, assess risk and existing coverage before purchasing separate bike insurance.

Do e-bikes require special insurance?

Yes. Many insurers treat e-bikes differently due to motor power and battery components. Check for motor-coverage limits, speed thresholds, and whether the policy explicitly covers e-bike models and upgrades.

E-bikes often need special coverage due to motors and batteries.

How do deductibles affect premiums?

Higher deductibles usually lower premiums, while lower deductibles raise them. For bikes, also consider how deductible interacts with theft or total-loss payouts and whether there’s a separate deductible for gear.

Higher deductibles lower premiums but raise out-of-pocket costs at a claim.

Can I insure multiple bikes under one plan?

Many providers offer multi-bike policies or rider options for multiple bicycles. Bundling can yield discounts, but confirm per-bike limits and whether all bikes are covered identically.

Yes, you can often bundle multiple bikes under one plan.

What is the typical claims process like?

Most insurers require proof of ownership, photos, receipts for upgrades, and sometimes a police report for theft. Timelines vary; quicker claims come with clear documentation and prompt communication.

Claims usually require ownership proofs and documentation; timelines vary.

Quick Summary

- Define riding patterns and storage to pick between standalone vs rider

- Compare coverage types and per-bike limits across providers

- Check deductibles and their impact on long-term costs

- Document bike value and components to speed claims

- Explore bundling and discounts to maximize value