How Much Does Bicycle Insurance Cost? A Practical Guide

Explore typical bicycle insurance costs, what drives premiums, and practical steps to save. A BicycleCost guide covering basic vs. comprehensive coverage, policy factors, and discount tips.

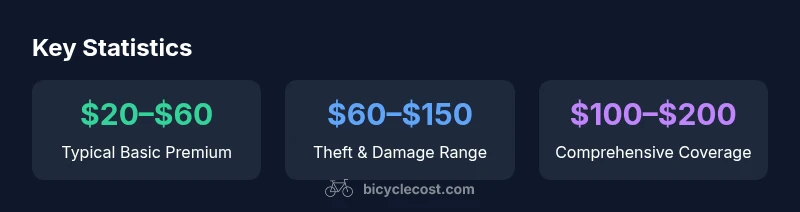

According to BicycleCost Analysis, 2026, most riders pay between $20 and $60 per year for basic bicycle insurance. Comprehensive coverage can push the annual cost higher, typically in the $60 to $150 range depending on bike value and policy limits. Your actual price hinges on coverage, deductible, rider risk, and location.

Understanding what bicycle insurance covers

Bicycle insurance policies vary, but most plans are designed to protect you from three core financial risks: theft, damage, and third-party liability. Theft coverage compensates you when your bicycle is stolen or confiscated from secure storage; damage coverage helps repair or replace your bike after accidents, vandalism, or even some weather-related incidents; liability coverage protects you if you injure someone or damage property while riding, potentially covering legal costs up to policy limits. Many policies also extend to personal belongings such as helmets, lights, or GPS devices that are damaged or stolen along with the bike, and some add-ons cover emergency transport if you’re stranded far from home.

The level of coverage you need depends on your bike’s value, how you ride, and where you store it. The BicycleCost team found that riders with high-priced or custom builds typically opt for higher limits and more robust theft protections, while casual riders may be comfortable with basic liability plus theft. It’s essential to read each policy carefully because coverage gaps—like vandalism exclusions or limited off-street use—can undermine protection when you need it most. In short: align coverage with your usage, risk, and budget.

Key factors that affect your premium

Premiums are driven by a combination of bike characteristics, rider behavior, and policy structure. High-value bicycles, such as custom builds or high-end road bikes, generally command higher premiums because the replacement cost is greater. Your location matters: urban cores with higher theft rates often lead to larger premiums, while secure storage areas can reduce costs. Security plays a big role: investing in quality locks, a monitored storage solution, or GPS tracking can lower risk in the insurer’s eyes. Usage matters too: daily commuting in dense traffic raises exposure, whereas weekend leisure riding might yield a lower rate. Coverage limits and deductibles also shift price: higher limits raise cost, while a higher deductible typically lowers it. Finally, bundling with other policies (homeowners, renter’s, or auto) can produce meaningful discounts, as can multi-bike policies and seasonal adjustments in riding patterns. The goal is to balance protection with budget while reflecting your actual risk.

Coverage types and price ranges

Most riders choose among three broad coverage structures. Basic liability only covers damage you cause to others and their property, typically at the lowest price tier. Theft and damage coverage adds protection for your own bike against theft, vandalism, and accidental damage. Comprehensive coverage combines liability, theft, and damage, often with optional add-ons for accessories and medical payments. Price ranges vary by bike value, location, and insurer, but common guidelines place basic coverage in the $20–$60 range annually, theft/damage around $60–$150, and full protection roughly $100–$200. Electric bikes may incur higher premiums due to battery and motor risks. Always verify how each policy defines covered risks, exclusions, and claim processes. The exact figures depend on the insurer and your circumstances, so quotes are essential for accuracy.

How to estimate costs for your bike

Start by determining your bike’s value and the level of protection you want. List essential accessories (lights, smart devices, saddle bags) and decide whether you need coverage for those items as well. Consider your riding habits: daily commuting in a crowded city warrants stronger theft protections and higher liability limits than occasional weekend rides. Get quotes from at least three insurers, noting deductibles, coverage limits, and bundled discounts. If your bike is high-value (roughly above a few thousand dollars), seek an appraisal or a rider endorsement to ensure your coverage reflects replacement costs. Use online calculators, but always confirm with a live agent to verify what is and isn’t covered. Document bike serial numbers, proof of ownership, and any upgrades to streamline claims.

Discounts, deductibles, and savings

Premiums rise with lower deductibles, higher coverage limits, and more add-ons. If you want to save, consider raising your deductible within a comfortable range and asking about multi-policy discounts. Security investments—a certified lock, indoor storage, and GPS tracking—can lead to lower premiums. Some insurers offer discounts for riders who take safety courses or participate in local cycling programs. If you own more than one bicycle, inquire about multi-bike discounts or a single policy that covers all bikes. Review whether add-ons like accident forgiveness or claim-free discounts apply to your situation. Small changes in your risk profile can translate into noticeable annual savings over time.

Real-world scenarios by bike type

Road bikes and high-end mountain bikes typically justify higher premiums due to replacement costs and specialized components. For a basic commuter bike, a simple liability and theft plan may be sufficient. Electric bikes (e-bikes) generally require higher coverage limits because of battery and motor risks, plus possible charging liability. A customized bike with rare parts or a vintage frame might benefit from tailored endorsements to ensure full replacement value. Insurance for accessories—racks, panniers, lights, and GPS devices—can be included or sold as separate riders, depending on the policy. Consider your usage profile and the specific risks of each bike type when choosing coverage.

Authoritative sources and methodology

Policy pricing is inherently variable and depends on jurisdiction, insurer practices, and individual risk factors. To guide our recommendations, we review industry guidance from major publications and regulatory bodies. Our approach combines quoted ranges from multiple providers with general market trends and the substitution effect of security investments. We also compare coverage definitions, exclusions, and claims processes across carriers to help riders understand what’s truly included. For further reading and verification, consult the sources listed in the methodology section below. The BicycleCost team emphasizes using real quotes and tailoring protection to your actual riding style and bike value.

Practical tips for selecting a policy

- Start with coverage that matches your bike’s value and how you ride.

- Prioritize theft protection if you park in urban areas or public spaces.

- Consider a higher deductible to reduce yearly premiums if you don’t expect frequent claims.

- Check for bundled discounts and multi-bike options.

- Confirm that accessories and high-value components are included or add a rider if needed.

- Review exclusions, such as unapproved storage locations or off-road use limitations, to avoid surprises during a claim.

Comparison of bicycle insurance coverage types and typical price ranges

| Coverage Type | Typical Premium Range | What It Covers | Notes |

|---|---|---|---|

| Basic liability | $20–$60 | Liability to others in accidents; property damage up to policy limit | Usually the cheapest option |

| Theft and damage | $60–$150 | Theft, accidental damage, vandalism; applies to bike and accessories | Common add-on for most riders |

| Comprehensive coverage | $100–$200 | Theft, damage, plus liability protection; may include accessories | Higher limits and added protections |

| E-bike coverage | $120–$250 | Theft, damage, and liability for electric bikes; battery risks included | Higher due to powertrain risk |

People Also Ask

What factors influence bicycle insurance costs?

Premiums depend on bike value, rider location, storage, usage, coverage limits, and deductibles. High-value bikes or urban riding tend to cost more, while robust security and multi-bike policies can reduce rates.

Costs vary with bike value, where you ride, and how you store it. Security and usage patterns matter when you compare quotes.

Do I need bicycle insurance if I already have homeowners or renters insurance?

Homeowners or renters policies may offer limited bicycle coverage but often don’t cover high-end bikes or theft outside the home. A dedicated bicycle policy usually provides clearer coverage terms and higher limits.

Your home policy might not cover everything. A dedicated bike policy can fill gaps for theft and high-value parts.

Are e-bikes more expensive to insure than standard bikes?

Yes. E-bikes typically require higher premiums due to powertrains and battery risk, plus potential liability when charging or transporting. Check if the policy has separate e-bike terms.

E-bikes cost more to insure because of the battery and motor risks.

How much coverage should I buy?

Match coverage to replacement value and risk exposure. For expensive bikes, seek higher limits and consider full theft and damage protection. For casual riders, basic liability plus theft may suffice.

Match coverage to your bike’s value and how you ride.

Can I get discounts for security devices or bundling?

Yes. Locks, indoor storage, GPS trackers, and bundling with other policies can lower premiums. Ask insurers about specific security-based credits.

Security devices and bundling can shave your premium.

Can I insure a bike I haven’t bought yet?

Some insurers offer flexible terms to cover a bike you plan to purchase, but you’ll usually need a reasonable estimate of value. Ask for endorsement options once you own the bike.

You can often arrange coverage for a bike you plan to buy, but check with the insurer.

“The core of fair bicycle insurance is understanding your bike’s value and how you ride. A thoughtful policy reflects real risk, not just a sticker price.”

Quick Summary

- Compare quotes from at least three providers to benchmark pricing

- Increase deductible to reduce annual premiums if you can afford higher out-of-pocket costs

- Higher bike value and urban riding generally raise costs

- Security devices and multi-bike discounts can lower premiums

- The BicycleCost team recommends tailoring coverage to your actual riding and budget